With interest rates at historically low levels, these are bad times to be a saver.

The Bank of England base rate has been 0.5% or less for over a decade, and now stands at just 0.1% – and there’s even talk of possible negative interest rates.

Savings account providers have been reducing their rates on traditional accounts, so that it’s becoming increasingly difficult to find a savings vehicle that will beat, or even just match, the Retail Prices Index rate – currently 0.5%.

A recent report from financial analysts Moneyfacts found that between 1 March and 1 August 2020, the average easy access saving rate in the UK fell from 0.57% to 0.22%.

This means that, while a savings account offers a risk-free way of investing, the value of your savings is actually decreasing over time as inflation reduces the purchasing power of your money.

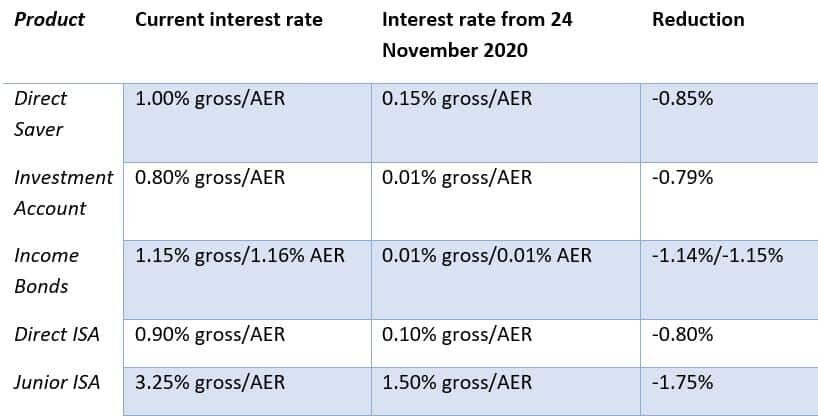

National Savings & Investments (NS&I) have recently become the latest provider to cut the rates on their savings products.

From November, only their Junior ISA will have an interest rate that beats inflation. An interest rate of 0.01% on the NS&I Investment Account means an annual return of just £1 on £10,000 invested.

In addition to these interest rate reductions, the amount of Premium Bonds prize money has been reduced by more than 25%, and the number of prizes by one million each month. This has the effect of reducing the prize fund rate from 1.40% to 1%.

So, with cash savings rates now generating a derisory return, and inflation continuing to eat into the value of savings, could now be the time to consider stocks and shares as an alternative investment option?

Stock market investment – key factors

There are three key factors to consider when it comes to investing in stock markets:

- Time

An old investment adage states that ‘it’s not timing the market, it’s time in the market’. This means that the longer you invest, the more likely it is that you’ll make a profit. So, you should only really consider investing if you’re happy to have that money tied up for the medium to long term – five years or more.

According to the detailed 2019 Barclays Equity Gilt Study, the stock market has outperformed cash in 69% of two-year periods, but if you extend the term up to ten years, the percentage of times stock markets outperform cash rises to 91%.

If you think you’ll need your money in the next five years, you should typically hold this as cash or very low-risk investments. But if you’re happy to tie it up over that period or longer, then stock market investment could result in very favourable returns on your money.

- Risk

Investing in the stock market has an element of risk. The value of your investment can go down as well as up and you may not get back the full amount you invested.

Past performance is not a reliable indicator of future performance. If you do not want to take any risk whatsoever with your money, then you may be better served with a savings product such as those offered by NS&I.

There are ways you can mitigate risk when you’re investing, such as:

- Not putting all your investment in one particular company or investment market sector

- Reinvesting dividends paid out on any of the stocks you own

- Using specialist funds that hold a mix of stocks along with other, lower risk investments such as gilts and bonds.

- Proportion

Investing doesn’t have to be an ‘all-or-nothing’ decision between stocks and interest-bearing savings accounts. It may well be prudent to keep a proportion of your savings in low-risk accounts – especially any money you know you’ll need to access in the next five years – while investing the remainder in stocks.

If your goal is to simply beat the current inflation rate of 0.5% with your investments, you could hold half of your money in an easy access savings account, paying around the 0.22% interest rate we referred to earlier, and therefore only need investment growth of 0.78% on the other half of your money to beat inflation.

Cash v shares in the long term

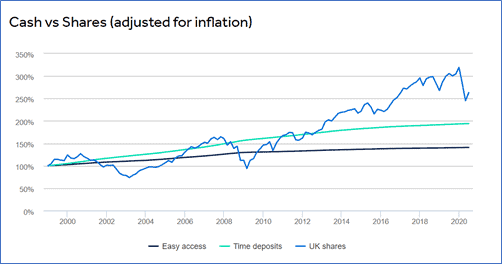

Since January 1999, when the Bank of England began recording data on effective interest rates, returns for savers in the average easy access account have failed to keep up with inflation.

Here’s some data from the last two decades that compares the returns from cash, time deposits, and shares.

Source: HL

As you can see, fixed-term savings accounts, where you lock your money away for a set period, have done better than standard ‘instant access’ savings accounts. Between January 1999 and June 2020, £100 grew to £194, or £128 after inflation.

In contrast, over the same period, the stock market turned £100 into £432 before costs. This works out to £284 after inflation. This is despite some very volatile periods, including the 1999/2000 dot-com bubble, the 2008 global financial crisis, and the recent Covid-19 pandemic.

So, if you’re prepared to invest for the medium or long term, stocks and shares could give you a better chance of outperforming inflation and meeting your financial goals.

Stock markets remain attractive for many investors

Another well-known investment saying is that ‘markets hate uncertainty’. So, it would be perfectly understandable if the recent volatility in investment markets caused by the Covid-19 pandemic, and the uncertain future, makes you reluctant to consider investing any of your savings in stock markets.

However, even in a recession, and even with a reasonable level of volatility, stock markets can remain an attractive option for investors.

With the UK Base rate at just 0.1% (and potentially going lower) and yields on government-backed investments such as gilts falling, markets continue to provide a good place for people to invest their money.

Larger blue-chip UK corporations typically operate internationally, which means they are often technologically capable and well-positioned to compete in an environment of social distancing.

In addition, in a normal year, about 70% of the revenues generated by FTSE 100 companies come from overseas and so the performance of the UK economy does not always have a significant impact on profits.

Also, bear in mind that you aren’t tied to a single stock in one company when investing in stocks and shares. You can reduce your investment risk by spreading your investment across different companies or even different investment markets. In this way, a big downturn in one particular company or sector can be offset by growth in others.

Stock market investment remains an attractive option for medium to long-term investors, even in the middle of the deepest recession in history caused by a once-in-a-generation global pandemic.

Get in touch

If you’re concerned about the low rates on your savings and you want to explore alternatives, please get in touch. Email info@blueskyifas.co.uk or call us on 01189 876655.

Important note

The value of your investment (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be regarded over the longer term and should fit in with your overall attitude to risk and financial circumstances.