If you’re dreaming of retiring early, it could be a reality sooner than you think. Many workers eagerly awaiting their retirement date could afford to give up work earlier than anticipated.

But deciding when to give up work can be fraught with challenges. Nobody wants to retire a couple of years early, only to find out further down the line that it’s come at the cost of financial security in later life. On the other hand, if you’re ready to hand in your notice and can afford to comfortably support yourself, why wait?

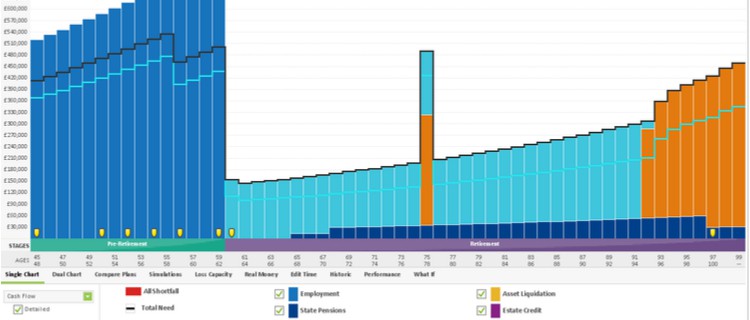

Cashflow modelling provides you with a way to understand when the time is right for you to retire.

Despite the rising State Pension age, many are choosing to retire early. In fact, six in 10 of those that gave up work in 2017 did so before their projected State Pension age or company pension scheme retirement date, research from Prudential found.

Being financially prepared for retiring early is crucial.

- 60% of those that were planning to retire early believe their finances were in order

- 86% had saved into a pension scheme throughout their working life

- 70% had spoken to a professional financial adviser before making a decision; this compares to 57% of those planning to give up work on their retirement date

However, the research revealed that overall those retiring early would be worse off financially. On average, retiring early costs £1,250 a year. As a result, understanding how much income you can expect from your retirement provisions is crucial; whether you want to give up work now or in 10 years.

This is where cashflow modelling can be an invaluable tool.

The benefits of cashflow modelling

There are two key benefits to cashflow modelling that can help you understand whether you can afford to retire now:

1. It gives you a graphic representation of your financial future

It can be difficult to understand how your retirement provisions will change over time; particularly when you begin to factor in areas like investment growth.

Cashflow modelling gives you a visual representation of how your finances will be affected, from early retirement through to the later years. With this in mind, it’s far easier to grasp how your wealth will be affected over time and the level of income you can afford to take.

If you’re thinking about retiring early, it gives you a clear insight into how this will affect the money you have to live on. Should you be unsure whether you can afford to retire sooner, it can give you the confidence to move forward with your plans.

After using cashflow modelling you might be surprised at the date when you can afford to comfortably retire.

2. It gives you an insight into how life events will have an impact

Life rarely follows the exact path that you plan, and that doesn’t change in retirement. Even when you’ve given up work, you’re likely to experience big life events that will affect your retirement plans.

Some of these milestones will inevitably influence your finances. By building these into cashflow modelling, you’ll be able to understand the level of impact they will have on your income. It gives you an opportunity to see how planned decisions, such as downsizing, will alter money in retirement. In addition, you can forecast events that may occur, for example, receiving an inheritance or going into long-term care.

Using cashflow modelling means you can have more confidence in your plans. But it goes beyond that. It’s a process that can give you the certainty that you’ll be able to overcome life’s financial obstacles once you retire.

The drawbacks of cashflow modelling to consider

There are disadvantages to consider when using cashflow modelling too:

1. It’s a static tool without regular reviews

As we’ve already mentioned, life is rarely linear. Even the best-laid retirement plans can go off course. In some cases, this may mean your income forecast will be vastly different from reality.

Cashflow modelling is a static tool without regular reviews. To remain useful throughout your retirement years, you’ll need to update the information regularly. The good news is that frequently reviewing cashflow modelling keeps it on track.

Whether your financial situation has improved thanks to an inheritance or changing aspirations mean you want to take a greater level of income now, keeping your data up to date is an important step.

Basing decisions off cashflow modelling that was created using old information may mean you’re not as informed as you think. As a result, reviewing cashflow modelling at set intervals should be considered crucial.

When updating information, it’s the perfect time to evaluate what your retirement goals are too. Perhaps in your retirement years, you’ve found you can live on a lower income but want to leave a greater legacy for your family. Or maybe you want to factor in greater care costs as you approach the later retirement years.

Cashflow forecasting can give you invaluable information but you should realise that as your circumstances change this will impact how useful it is unless reviews are undertaken.

2. It’s only as good as the data

Updating a cashflow modelling tool brings us on to the second drawback; it’s only as good as the data that’s input.

Incomplete or inaccurate information is, in turn, going to lead to unreliable forecasts. On top of that, the information that’s delivered will depend on the adviser’s interpretation of your finances and aspirations.

For this reason, it’s important to firstly provide as much accurate data as possible when starting the cash flow modelling process. And, secondly, to work with an adviser that understands what you want to achieve.

If you want to understand if you can afford to retire now, please contact us today. We’ll use our expertise and vast experience to use cashflow modelling to help give you the information you need to make decisions on your retirement date.