On 5 August, global markets posted significant drops amid mounting fears of a US recession.

That month, data from the Bureau of Labour Statistics indicated a rise in US unemployment and federal interest rates also remained high, prompting many analysts to predict that the US economy would slip into recession.

The knock-on effect was significant, and markets in the UK, the US, South Korea, China, Australia, Germany, Hong Kong, and more, fell in response.

The Nikkei 225, Japan’s benchmark index, made headlines by experiencing its steepest drop in nearly 40 years. Yet, to the astonishment of investors, the very next day the Nikkei rebounded with record-breaking gains.

The volatility of those 48 hours is a good example of how short-term fluctuations are inherent in investing. There are also lessons to be learned about how to ensure you minimise the effects of such volatility on your portfolio.

Read on to learn how frequently markets experience significant dips, and what you can do to ensure you are prepared for such volatility and downturns.

Global markets experience significant dips more often than you might think

During the dip in August, the Nikkei 225 fell by 12%, marking its biggest decline in 37 years and the heaviest one-day fall since the Black Monday crash in 1987. However, the following day, the index rose by more than 10%, reversing most of the previous day’s losses.

While the swift fall and rebound of the Nikkei was historical, declines of 10% or more are not uncommon and happen in global markets more often than you might think.

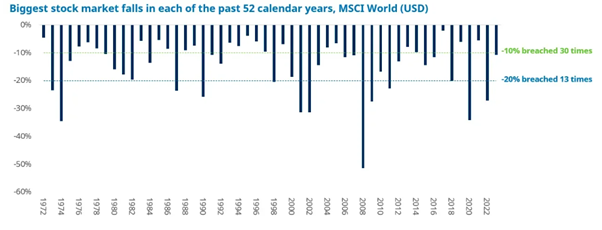

Research by Schroders revealed that global stock markets, as represented by the MSCI World Index, experienced declines of 10% or more in 30 of the past 52 years. More significant drops of 20% occurred in 13 of those years.

The graph below shows the biggest market dips since 1972 on the MSCI World Index.

Source: Schroders

As you can see, global markets have dipped by 10% or more in more years than not since 1972.

Despite the frequency and significance of such dips, global markets have delivered strong annual returns across this period overall. Data published by Curvo shows the MSCI has had an average compound annual growth rate of 7.39% over the last 25 years.

This suggests that staying invested through market fluctuations and exercising patience during downturns can be an effective approach to achieving long-term success.

Historical analysis reveals that remaining patient and resilient amid market declines is typically a more successful strategy than liquidating

Past performance is never a reliable indicator of future outcomes, but further research by Schroders reveals that liquidating investments during historical downturns would likely have resulted in long-term losses.

In an analysis of perhaps the two best-known stock market crashes in the past century, Schroders found that during both the Wall Street Crash and the 2008 financial crisis, investors who sold their stocks and moved to cash would have waited much longer to recover than those who stayed invested.

Investors who exited the market in 1929 at the start of the Great Depression would have had to have waited until 1963, 34 years, to break even from returns on their cash. While those who stayed invested would have experienced further losses at first, they would have broken even in 1945, 18 years earlier than those who liquidated.

Similarly, investors who exited the market during the 2008 financial crisis would still not have broken even today in 2024. On the other hand, those who remained invested would have again initially suffered further losses, before recovering around 2013.

During market downturns, it’s easy to let emotions or investor biases drive decisions to abandon stocks in favour of cash. However, the historical data suggests that liquidating your holdings amid declines has generally proven to be a poor long-term strategy.

So, staying patient and resilient during market dips and fluctuations has typically been a more effective strategy for achieving long-term stability and success than selling off your investments.

Portfolio diversification can help protect you against downturns and open you to wider returns

Portfolio diversification is another strategy crucial for managing risk, limiting losses, and enhancing your potential for capturing wide-reaching returns.

By spreading your investments across a range of asset classes, sectors, and regions, you reduce your exposure to the volatility of any particular market. It also opens you up to a range of markets that could enhance your potential for capitalising on diverse opportunities.

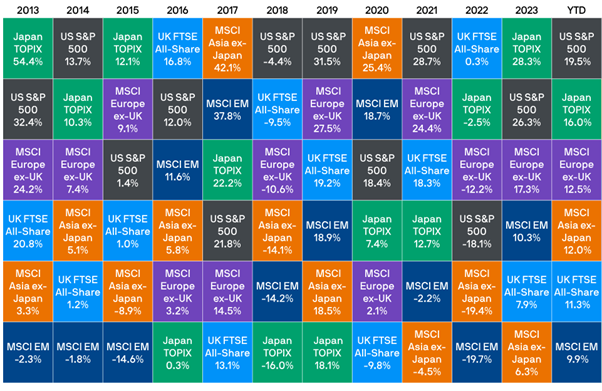

The table below shows the annual performance of a range of global indices for the last decade.

Source: JP Morgan

As you can see, it is almost impossible to predict which markets will perform well or badly from year to year. For example, Japan’s TOPIX was the strongest performer for three years and the weakest for four.

By diversifying your portfolio – in this instance, across multiple regions – you reduce the impact of market downturns and position yourself for broader returns.

For example, had all your investments been confined to the UK FTSE All-Share in 2020, you would have probably suffered considerable losses. But if you spread your investments across different indices and regions, you would have likely made gains as other markets performed markedly better than the UK that year.

So, diversifying your portfolio can lead to more stable investments, helping to cushion your holdings against significant declines like those experienced in August.

Get in touch

A financial planner can work with you to find ways of diversifying your portfolio and building a long-term strategy to help protect you from future volatility.

To speak to a financial planner, get in touch.

Email us at info@blueskyifas.co.uk or call us on 01189 876655.

Please note

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.