Earlier this summer, we looked at the recent Pensions Advisory Group report and highlighted some occasions where it might not be necessary for your clients to speak to a pension expert when they divorce.

On the flip side, there are sometimes many good reasons for taking financial advice early on in pension sharing cases. This is particularly true with larger and more complicated schemes.

One of the reasons why speaking to an expert is worthwhile is where there are issues regarding the Lifetime Allowance. This allowance is not increasing as fast as pension scheme valuations, so more and more of your clients will be affected.

While it has been possible for an individual to seek protection against the LTA over the years, with a total of seven different incarnations to date it is certainly a complex area!

A recent case we advised on highlighted how important specific financial advice can be to some cases. Although this was a particularly large case, the principles apply to many others. Crucially, advice and action needed to be taken before any pension sharing was implemented.

The Lifetime Allowance (LTA)

The LTA limits the value of an individual’s total pension benefits over their lifetime, with a tax charge on the excess over the LTA when benefits are taken.

The standard LTA is currently £1.03 million and is indexed annually based on the CPI. The LTA applies to both defined benefit and defined contribution schemes.

In addition, there are many ways in which an individual can have an enhanced LTA. It’s a complex area with different levels and forms of protection available.

The situation

Howard and Wendy (both age 65) are divorcing after a long marriage. Howard has a Self-Invested Personal Pension (SIPP) worth £4.7 million, which, as yet, has not paid any benefits (i.e. the fund is uncrystallised).

Howard applied for Enhanced Protection in 2006 meaning that he would never pay any LTA tax charge, provided that no further pension contributions were ever made.

His tax-free cash entitlement from this scheme is 25% of the LTA in 2006 (i.e. 25% of £1.5 million = £375,000).

Wendy has no pension scheme other than entitlement to the State Pension.

The issue

The issue here is that if Wendy receives 50% of Howard’s pension (her share = £2.35 million), she would be subject to an LTA test when taking benefits.

The current LTA is £1.03 million and any fund value over this level (£1.32 million, in this case) will be subject to a tax charge.

Tax-free cash availability is 25% of the current LTA (£257,500).

There are two options regarding how the LTA tax can be dealt with:

- A tax charge of 55% on the amount above the LTA (Tax = £726,000). The balance over the LTA is then paid to the member. In this case, this equates to £594,000 as a cash lump sum.

- Tax at 25% on the excess over LTA (Tax = £330,000). The balance over the LTA (after 25% tax) is effectively added to the pension and withdrawals are taxed as income.

Note that, in mathematical terms, the above two options result in similar figures after tax. This is because withdrawals from the remaining fund (in option 2) will be subject to Income Tax but will depend on individual circumstances.

Both Howard and Wendy will have a further (and final) LTA test at age 75. Howard will be exempt from any further tax, however, Wendy will be subject to LTA tax on any growth in the fund since the last LTA test and this will include withdrawals taken along the way.

The solution

If Howard takes the maximum tax-free cash from the fund before sharing it, the remaining fund is deemed ‘crystallised’ and thus is tested against the LTA. As Howard has Enhanced Protection no tax is payable. This £375,000 tax-free cash could, of course, be shared with Wendy.

If Wendy then receives 50% of the remaining fund she will be awarded a ‘pension credit factor’ to recognise that the fund that she has received has already been tested against the LTA and thus should not liable for any LTA tax.

In this instance, this factor is 2.09. As this fund has already paid out tax-free cash to Howard, no further tax-free cash is available to Wendy, so the full pension fund is available to produce an income without any further LTA tax charge. As above, there is a further LTA test at age 75 although by using Wendy’s Pension Credit Factor this test will be on 2.09 (the LTA at age 75).

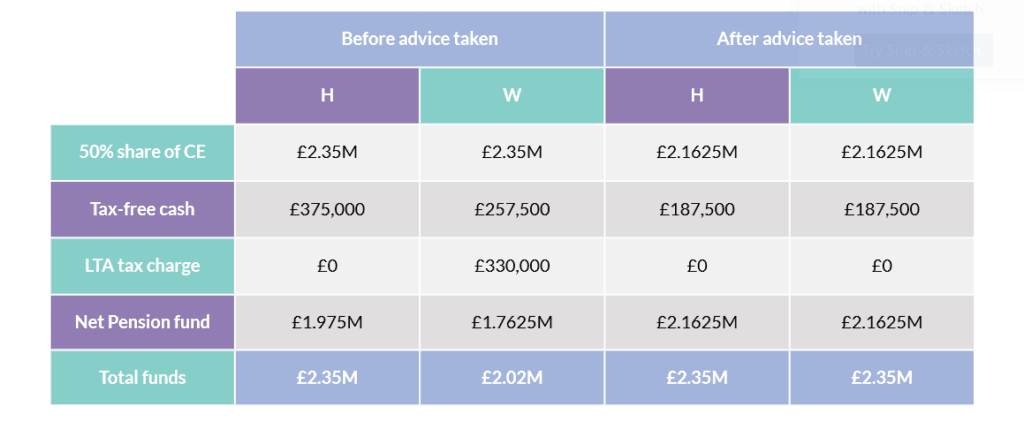

A summary

For the purposes of the grid below it is assumed that Wendy elects to pay a 25% LTA tax charge (option 2 above) and the remaining fund is taxed in the same manner as the rest of her pension scheme, i.e. Income Tax.

This method gives equitable pension fund sizes and taxation liabilities so was our preferred option from a pension sharing report perspective.

Taking advice as described above will have saved Wendy £330,000 in tax and created equal pension funds, income opportunities and taxation liabilities.

If you have clients who have complex pension arrangements and who may benefit from talking to a chartered financial planner, please get in touch. Email info@blueskyifas.co.uk or call us on 0118 987 6655.