One of the most common questions clients ask us is: “will I have enough to live on when I retire?”

Obviously, the answer to this question is highly personal to an individual or couple. It depends on what you intend to do once you retire, what standard of living you want, and how long you anticipate that your retirement will last.

Two recent pieces of research have considered how much you might need to live on to ensure a comfortable retirement. Again, these figures are based on different levels of “comfort” and what you expect to spend your money on when you have the opportunity to do whatever you wish.

Read on to find out more, and why many people are likely to be saving too little to achieve their desired retirement lifestyle.

90% of pension savers at risk of not generating sufficient retirement income

In recent years, pension provision has changed. In the past, many people were in more financially secure defined benefit (DB) pension schemes, which offered a gold-plated pension for life based on your salary and years of service.

Now, 2 in 3 employee contributions are to defined contribution (DC) schemes. And, a new report by the Centre for Ageing Better has revealed that around 90% of all DC savers are at risk of not achieving a decent “replacement rate” – the proportion of their pre-retirement income that their pension provides.

Findings by the Pensions Policy Institute (PPI) reveal that many over-50s approaching later life were at risk of missing out on an adequate retirement income, with 1 in 4 people at risk of not reaching the Joseph Rowntree Foundation minimum income standard.

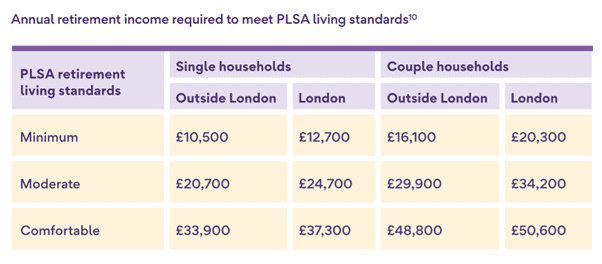

Just 1 in 3 people can expect a “moderate” retirement, and 1 in 10 a “comfortable” retirement under the Pensions and Lifetime Savings Association (PLSA) definitions:

- A “minimum” lifestyle would cover all needs, with some left over for fun and social occasions

- A “moderate” lifestyle would provide you with more financial security and flexibility

- A “comfortable” lifestyle would allow you to be more spontaneous with their money.

According to the PLSA, here’s what you’d need to earn to meet these various living standards:

In February 2021, Which? surveyed 6,800 retired and semi-retired people to establish what level of income they needed to achieve their retirement lifestyle. The results were broadly similar:

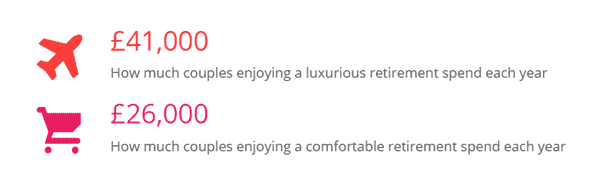

Here, a “comfortable” retirement covers all the basic areas of expenditure and some luxuries, such as European holidays, hobbies and eating out. As a couple you’d need £41,000 a year if you include luxuries such as long-haul trips and a new car every five years.

As you can see, couples would need an income approaching £50,000 a year to maintain a “comfortable” or “luxurious” lifestyle in retirement.

If you imagine that your retirement might last 20 or 30 years, you can see that this requires a significant pension pot to be able to afford this standard of living.

How much you’ll need to save for a comfortable retirement

As above, the amount you’ll need in your pension pot will be highly specific to you. If you plan to head off on holiday abroad, you’ll need more money than if you plan to be frugal and spend your vacations in the UK.

Which? has crunched the numbers to work out how much you might need to save to achieve a comfortable retirement.

If you were looking to achieve a comfortable post-tax income of £26,000 a year and wanted to get a guaranteed income paid to you via a joint-life annuity, you’d need a pot of £265,420, according to their calculations.

This assumes that you’ll receive an annual State Pension of around £16,000 as a couple, so you’d need to generate income from an annuity of around £10,000 a year.

To get the same amount from income drawdown, where your money remains invested and you draw a regular income, Which? say you’d need £154,700 in your pot, assuming that your savings grow by 3% annually.

If you wanted a more luxurious retirement and required a post-tax annual income of £41,000 (including the State Pension), you’d need an initial pot of around £757,000 to buy a joint-life annuity or £442,020 invested in income drawdown.

Get in touch

We’re here to help you to achieve the retirement you desire. We can work with you to ensure that you can build up the retirement fund that will support your lifestyle, and to help you to take your income in the most tax-efficient way.

To find out how we can help you, please get in touch. Email info@blueskyifas.co.uk or call us on 01189 876655.